What is a Sinking Fund vs Emergency Fund?

Are you new to budgeting? Are you trying hard to take control of your money?

I know how hard it can be to understand all the ins and outs of budgeting. Today we are talking about the Savings part of your budget.

If you’ve read my post about 50/30/20 Budget Rule then you are ahead of the game. In that post, I talk about how you should be saving for lots of different things. Two of these savings should be for a sinking fund and an emergency fund.

If you are brand new to budgeting check out my post about Budgeting Basics.

“A budget is telling your money where to go, instead of wondering where it went.” —

John C. Maxwell

Both of these funds are essential to a healthy budget.

Both of these funds may sound the same…but they are both used for different purposes.

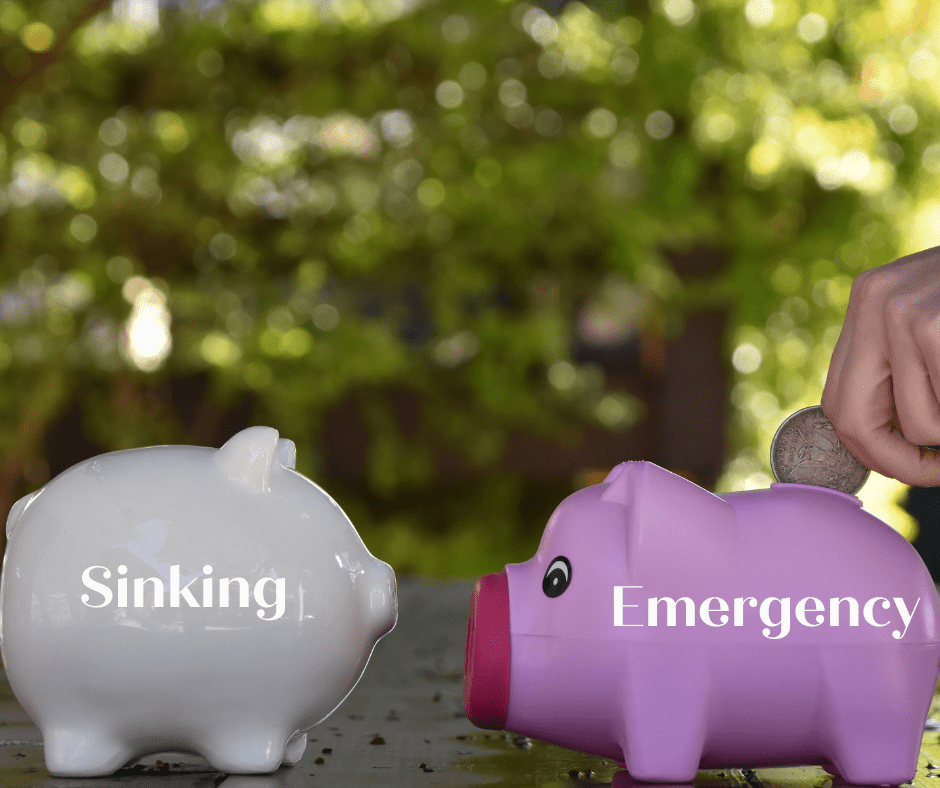

So what is a sinking fund vs emergency fund?

A sinking fund is a savings used for a specific purpose.

An emergency fund is exactly what is sounds like…an emergency fund.

Let’s talk about all the reasons that you should have both of these funds. Both of these funds can cushion you from going into debt. Protect you!

Let’s also talk about how to budget for these savings funds. And also who needs these funds the most.

Sinking Fund

So what’s the difference between a sinking fund vs emergency fund.

A sinking fund is a savings account set up for a specific reason. This type of savings can be for recurring expenses or planning for a future event.

Examples of a sinking fund:

- New Furniture

- New Appliances

- Vacation

- Christmas

- Car Repair

- New Roof

- Wedding

- College Fund

- House Renovation

Basically, anything that you want or need to do. This is a deliberate account.

A sinking fund will have a definitive start and stop date. You will choose a specific amount of money needed. You will figure out how much you need to contribute in a set amount of time.

A sinking fund is especially important for first-time homebuyers. I talk about this in mistakes that first-time homebuyers make. It is very important for homeowners to have a sinking fund for future repairs and maintenance.

“Beware of little expenses; a small leak will sink a great ship.” —

Benjamin Franklin.

Saving is not as hard as you think. Making small changes can really add up.

Don’t make this hard on yourself. Set up a certain amount of money monthly that you can afford to save. This money is separate from your retirement accounts, emergency fund, or investment account.

You should save this money in:

- High-Yield Savings Account: A high-yield savings account is the same as a standard savings account. But pays a much higher yield on your money

- Money Market Account: A money market account is an account that pays interest based on current interest rates in the money markets.

- Certificate of Deposit (CD): A CD is a savings account that holds a fixed amount of money for a fixed time. Typically 6 months, 1 year, or 5 years. In exchange, the bank pays interest.

Emergency Fund

When it comes to sinking fund vs emergency fund….an emergency fund is the most important one to have.

An emergency fund is money set aside for emergencies. The most common emergencies come from a loss of a job or a medical emergency

Over 60% of Americans are living paycheck to paycheck.

Life is difficult. You never know what is going to happen tomorrow. Setting up an emergency fund is one of the smartest decisions that you can make. No matter how much money you make, you need to be prepared.

How much do I need for an emergency fund? Most experts tell you to put away 3-6 months’ worth of living expenses.

Here’s a great breakdown of what you need for an emergency fund.

Your emergency fund is your safety net. You never want to touch this money except for emergencies.

Start on this fund today. Figure out what expenses you will have to keep paying. These are necessities, not luxuries. Write it down and come up with a number that you need to start working towards today.

This should be a top priority in your saving category. Once you have saved enough for your emergency fund, then you can start saving for your other categories.

By setting up both of these accounts you are preparing for your financial future. This won’t happen overnight, but you need to start working on this today.

Comments

Pingback: Mistakes First-Time Homebuyers Make-10 Common Mistakes

Pingback: 50/30/20 Budget Rule | A Simple Guide to follo

Pingback: Financial Habits | 14 Smart Financial Habits to Start Today

Pingback: Pay Off Debt | Step by Step Guide to Pay off Debt Quikly